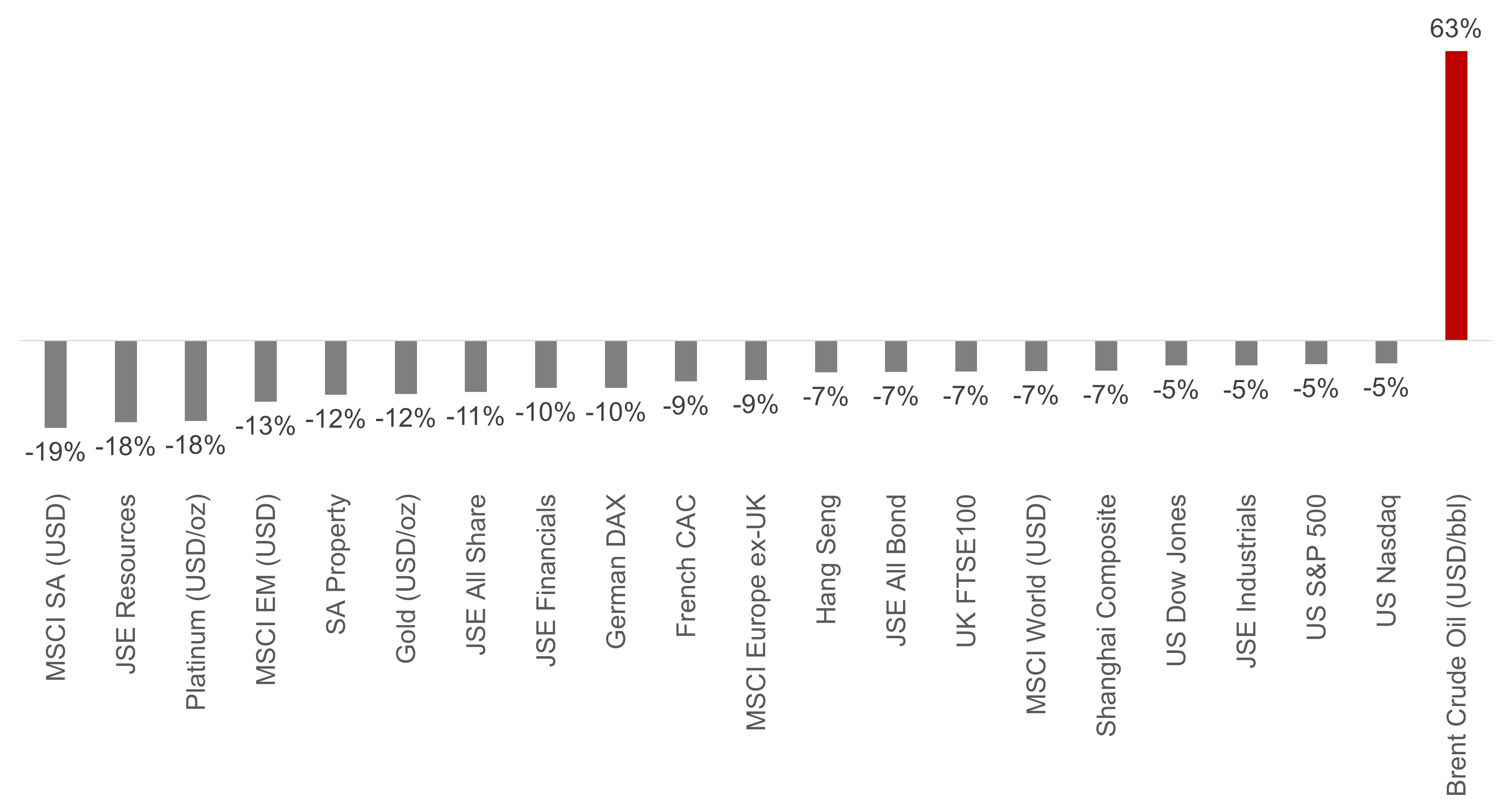

South African equities experienced a sharp reversal in March, ending a twelve-month winning streak as global shocks and commodity weakness weighed heavily on local assets. The FTSE/JSE All Share Index fell -11.2% MoM, marking its worst monthly performance since the Covid crisis in 2020, while the FTSE/JSE All Bond Index declined -6.8% MoM amid a sharp rise in yields. SA-listed property also came under significant pressure, falling -11.8% MoM, as all major asset classes ended the month in negative territory. The sell-off was broad-based, with the resources leading the decline (-17.8% MoM) as precious metal prices corrected sharply, followed by financials (-10.3% MoM) and industrials (-5.4% MoM). Precious metal miners, which had driven much of the market’s recent outperformance, were the largest detractors, with gold and platinum miners falling sharply in line with underlying commodity prices. In US dollar terms, MSCI South Africa declined -19.0% MoM, significantly underperforming both MSCI World (-6.6% MoM) and MSCI Emerging Markets (-13.3% MoM), as a weaker rand compounded losses.

South Africa’s macroeconomic backdrop became more uncertain in March as global developments introduced upside risks to inflation and interest rates. Although February inflation data remained benign, with headline and core CPI both easing to 3.0% YoY, the sharp increase in global oil prices shifted the outlook meaningfully. The South African Reserve Bank kept the repo rate unchanged at 6.75%, but struck a more cautious tone, highlighting the risk of second-round inflation effects and outlining scenarios that could necessitate future rate hikes. Bond markets reacted negatively, with the 10-year government yield rising sharply to around 9.3%, contributing to one of the worst monthly performances for local bonds on record. The rand weakened significantly, depreciating -5.9% MoM against the US dollar as global risk aversion intensified and investors rotated into safe-haven currencies.

Global markets were dominated by a sharp escalation in geopolitical tensions during March, triggering one of the most significant energy shocks in recent history. Military conflict involving the US, Israel and Iran, alongside the effective closure of the Strait of Hormuz, disrupted a critical global energy supply route and drove oil prices sharply higher. Brent crude surged, and ended the month up +63.3% MoM to over US$118/bbl, while global growth expectations weakened and inflation fears intensified. Global equity markets sold off broadly, with the MSCI World Index declining -6.6% MoM, its worst monthly performance in over three years. Rising energy prices and inflation expectations led markets to reassess the path of monetary policy, with expectations for rate cuts pushed out and bond yields rising globally. In contrast to the risk-off environment, precious metals declined sharply, with gold falling -11.6% MoM and platinum down -17.5% MoM, as higher real yields and a stronger US dollar reduced their relative appeal.

US equities declined meaningfully in March as geopolitical tensions, rising yields and weaker growth data weighed on investor sentiment. The S&P 500 fell -5.1% MoM, while the Nasdaq declined -4.9% MoM and the Dow Jones dropped -5.4% MoM, ending its ten-month winning streak. Markets were particularly sensitive to the inflationary implications of the energy shock, which drove US Treasury yields higher, with the 10-year yield rising above 4.4% before closing the month at 4.3%. The Federal Reserve kept rates on hold, emphasising uncertainty around the economic impact of geopolitical developments and the persistence of inflation risks. Economic data painted a mixed picture, with inflation broadly stable but growth slowing, as GDP was revised lower and labour market data surprised to the downside. Energy stocks were the clear outperformers, benefiting from the surge in oil prices, while broader equity markets struggled under tightening financial conditions and reduced expectations for policy easing. A flight to safety in the US greenback pushed the US Dollar Index up +2.4% MoM.

European equity markets were particularly hard hit by the energy shock, given the region’s reliance on imported energy. The MSCI Europe ex-UK index declined -8.6% MoM, marking its worst monthly performance since March 2019 when we had the COVID-19 induced market crash. Germany’s DAX and France’s CAC fell -10.3% and -8.9% MoM respectively. The UK market proved relatively more resilient, with the FTSE 100 declining -6.7% MoM, supported by its higher exposure to energy companies. Inflation in Europe edged higher, while economic growth remained subdued, reinforcing concerns around stagflation risks in the region as higher energy costs weigh on both consumers and industrial activity.

Emerging market equities also came under significant pressure, reversing much of their strong year-to-date performance. The MSCI Emerging Markets Index declined -13.3% MoM, underperforming developed markets as global risk aversion increased and capital flowed back into the US dollar. Commodity-producing markets faced mixed outcomes, with energy exporters benefiting from higher oil prices, while metal exporters were negatively impacted by falling prices. Chinese equity markets declined but were relatively more resilient than peers, supported by reduced dependence on Middle Eastern energy and signs of stabilisation in domestic economic activity. The Shanghai Composite fell -6.5% MoM, while the Hang Seng declined -6.9% MoM, as weakness in global risk sentiment outweighed improving macro data.

The hedge fund ended the month in negative territory, as detractors from the long book outweighed gains from the short book. Performance on the long side was primarily impacted by positions in Impala Platinum, Barrick Mining and Valterra Platinum, while Glencore was the main positive contributor. Within the short book, the largest gains were generated from index protection and positions in the gold mining and local property sectors, with minimal losses recorded across other positions.